Jump to: Forms, webinar recording & other resources

In this article, we show you how to produce the data you are looking for from our payroll system to fill out the long Form 3508.

The information is easily available in our CV-19 Dashboard, with keys that tell you which data element belongs where on the application. We have done our part in simplifying it so that you have the information available at your fingertips. It includes the capability to modify employee elements and reproduce the data as many times as you need.

- Before you proceed with this form, first determine if you are qualified to use either Form 3508S or Form 3508EZ, as these 2 forms are much simpler and easier to complete. See Can Your Company Use 3508S? as well as Can Your Company Use 3508EZ?.

- To ensure that the data we produce is complete and valid, you need to ensure that certain employee setups are correct. Some of these you might not have needed in the past, but they are important now as many figures are derived from them. See Payroll System Setups/History.

There are four parts to the long PPP loan forgiveness application:

- PPP Schedule A Worksheet

- PPP Schedule A

- PPP Loan Forgiveness Calculation Form

- Borrower Certifications

Although the actual forms are laid out in a different order, we intentionally lay it out this way as it will be easier to complete. Much of the data in the Loan Forgiveness Calculation Form is derived from the Worksheet and Schedule A.

Ready? Take a deep breath.. and let's get right to the task of applying for loan forgiveness. Rest assured that with all our tools, everything payroll-related is at your fingertips and will make this process a breeze. We are committed to providing you with outstanding support during the process.

PPP Schedule A Worksheet:

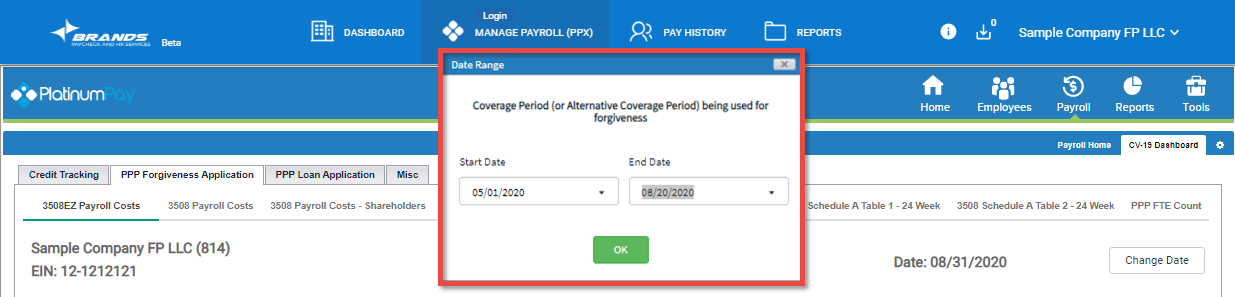

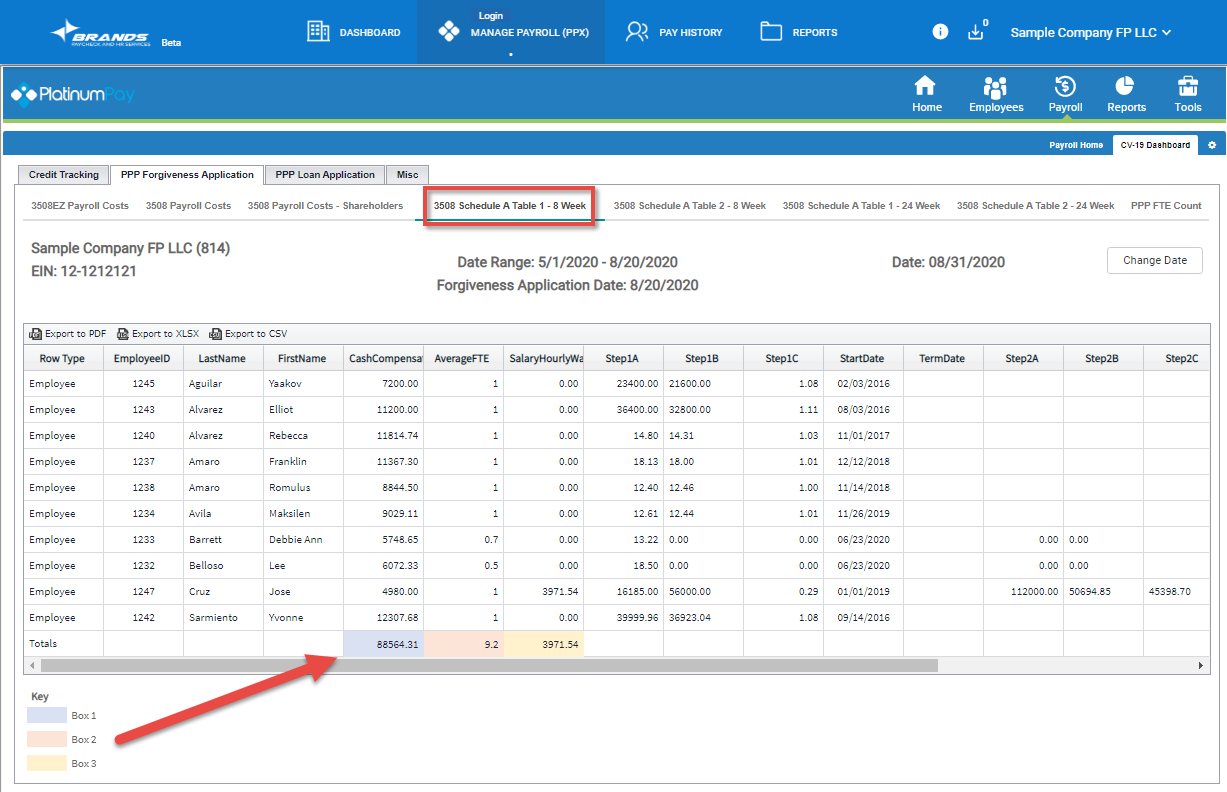

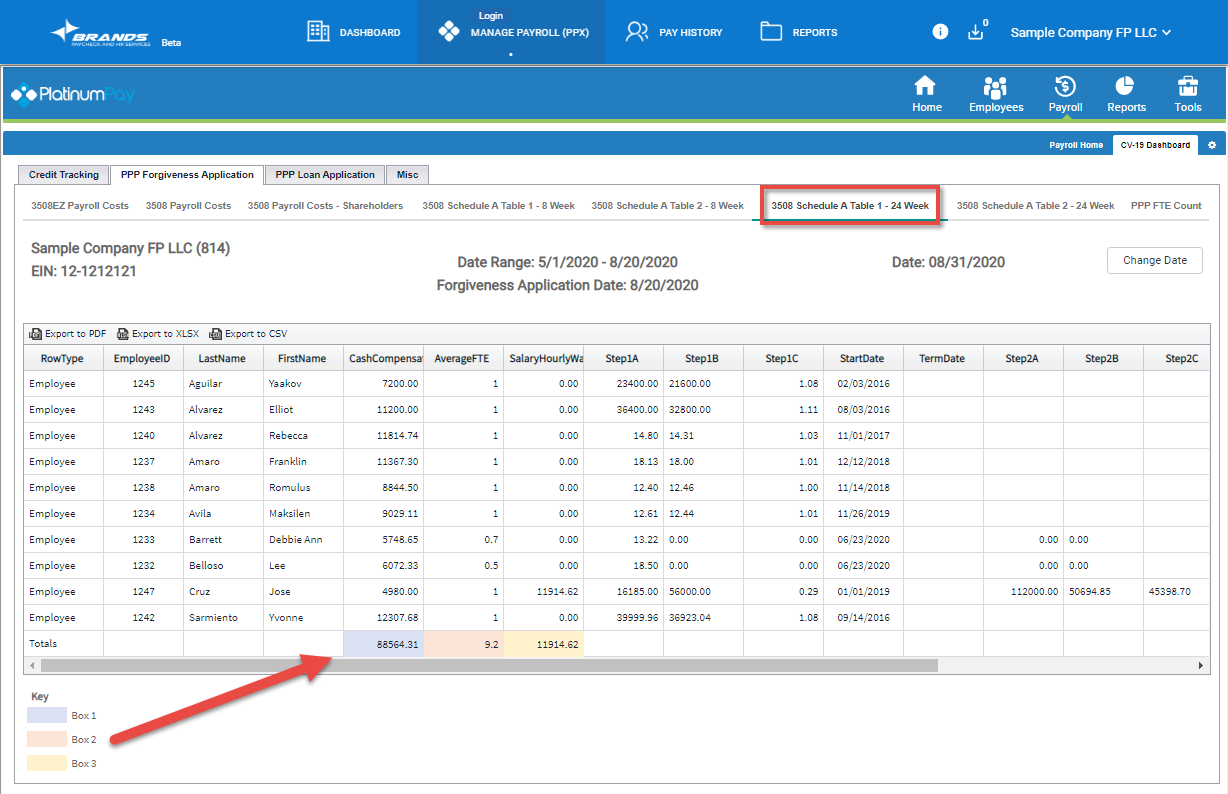

To fill out the PPP Forgiveness Calculation Form, begin by filling out the Schedule A Worksheet. Choose the Schedule A tables that match the forgiveness period you have selected, either 8-week or 24-week. When you run the report, plug in the date range for your coverage period or alternative coverage period.

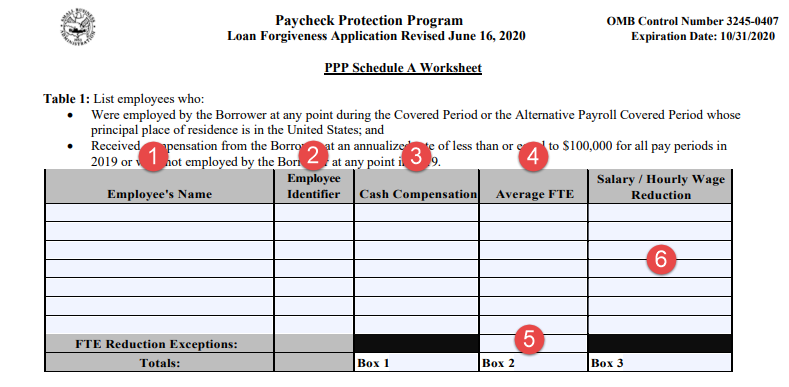

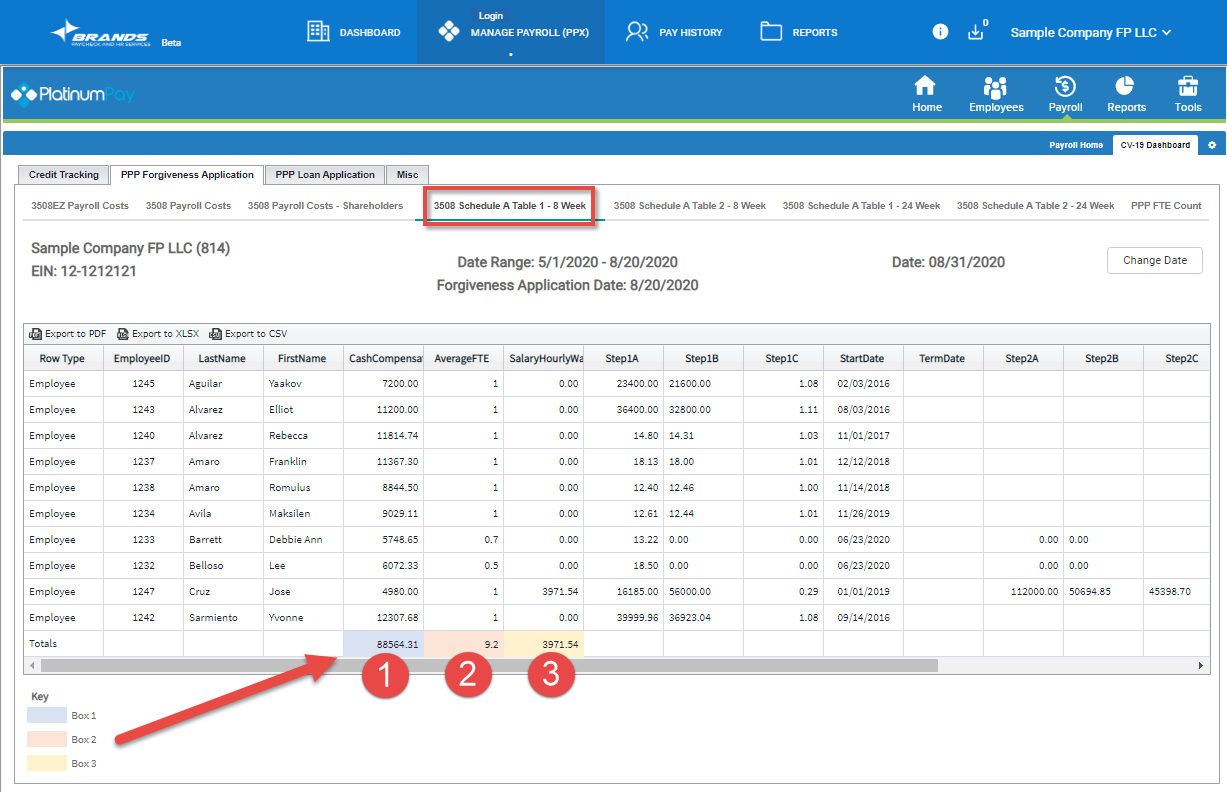

Table 1

How it looks on the form:

- List each employee, not including independent contractors, self-employed, partners and owner-employees.

- Last 4 digits of employee's social security number.

- Total paid to the employee during the Covered Period or Alternative Payroll Covered Period.

- Employee's average FTE during the Covered Period or Alternative Payroll Covered Period.

- For the FTE Exception info, see FTE Reduction Exceptions.

- For what you need to consider on the Salary Wage Reduction column, see Salary Wage/Hourly Wage Reduction.

How to get the info:

To get the data for Box 1, 2, and 3, use the data from "3508 Schedule A Table 1."

- Use the data from 3508 Schedule A 1 - 8 Week if you are using the 8 week period

- Use the data from 3508 Schedule A 1 - 24 Week if you are using the 24 week period

3508 Schedule A 1 - 8 Week

3508 Schedule A 1 - 24 Week

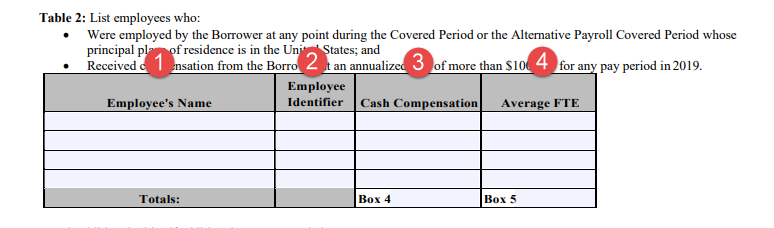

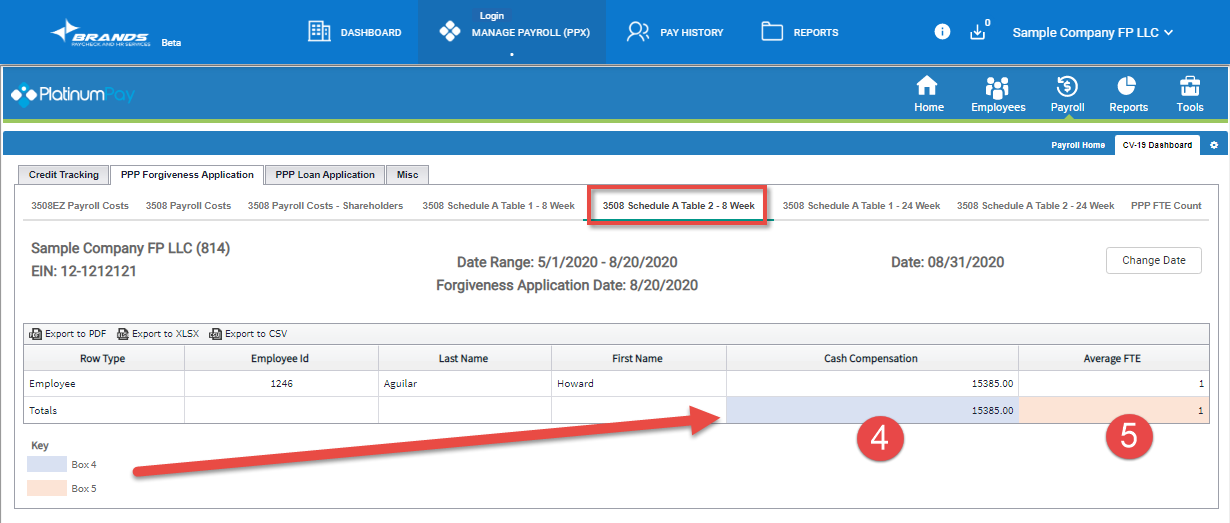

Table 2

How it looks on the form:

- List each employee, not including independent contractors, self-employed, partners and owner-employees.

- Last 4 digits of employee's social security number.

- Total paid to the employee during the Covered Period or Alternative Payroll Covered Period.

- Employee's average FTE during the Covered Period or Alternative Payroll Covered Period.

How to get the info:

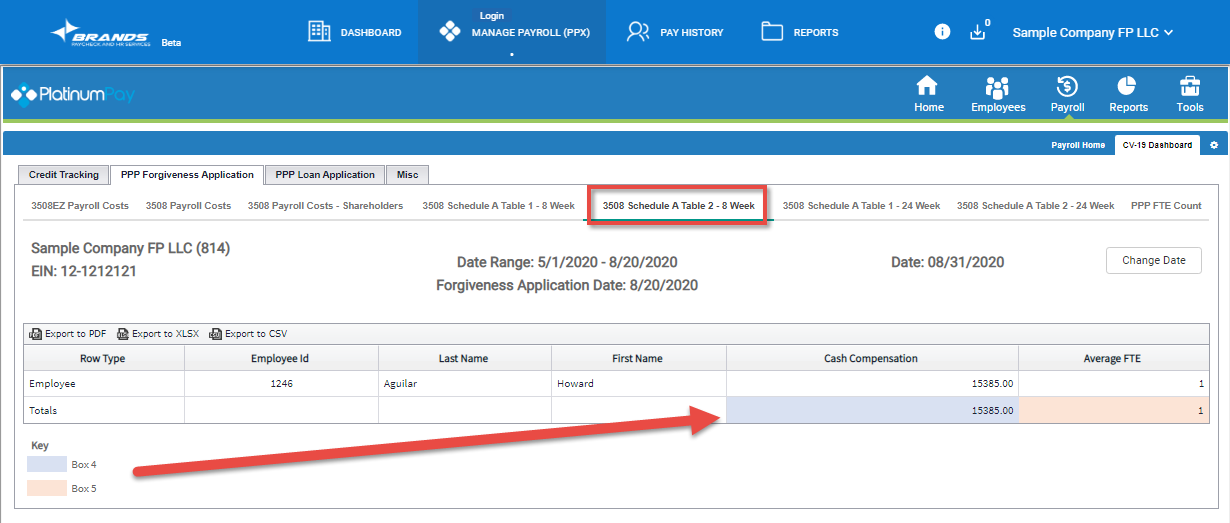

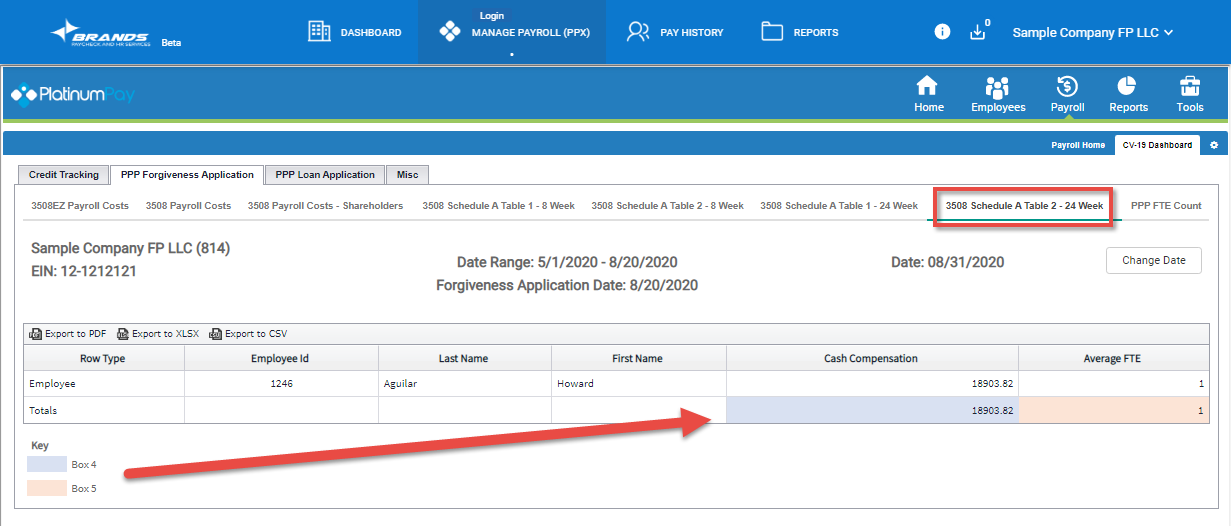

To get the data for Box 4, and 5, use the data from "3508 Schedule A Table 2."

- Use the data from 3508 Schedule A 2 - 8 Week if you are using the 8 week period

- Use the data from 3508 Schedule A 2 - 24 Week if you are using the 24 week period

3508 Schedule A 2 - 8 Week

3508 Schedule A 2 - 24 Week

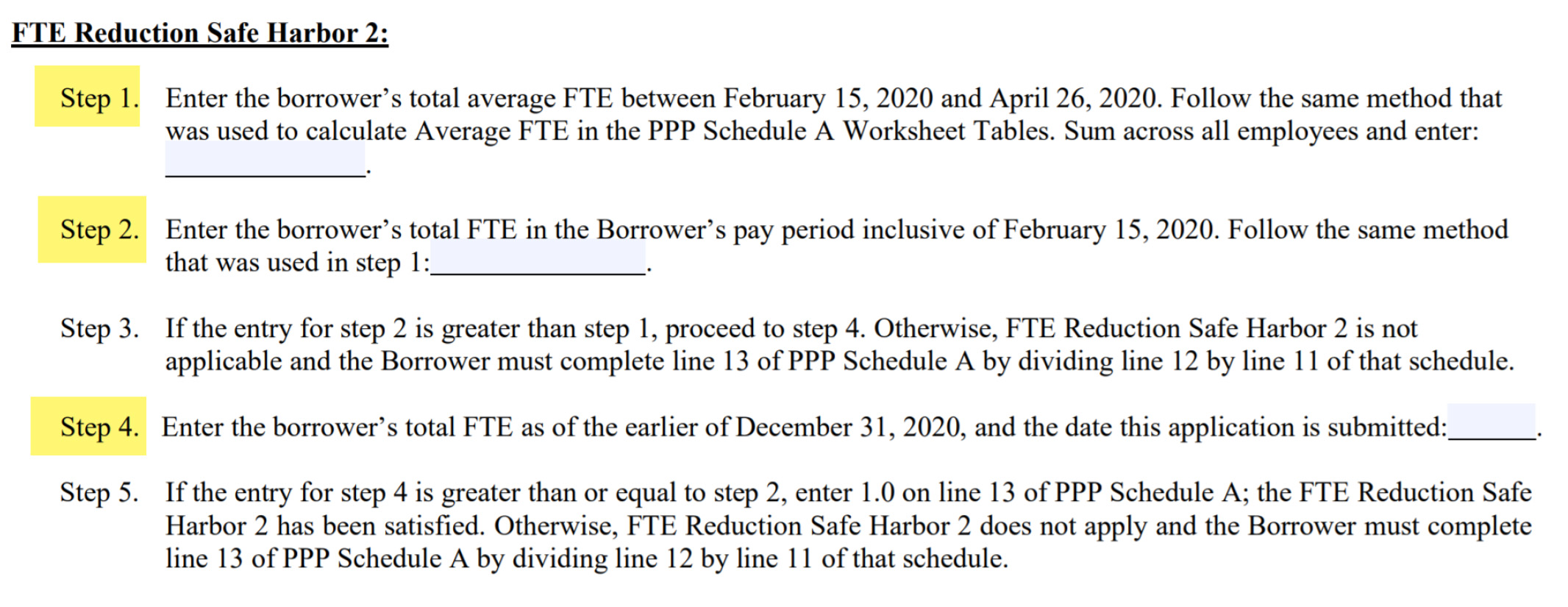

FTE Reduction Safe Harbor 2

Step 1: Use the PPP FTE Count report to calculate the FTE for the date range of 2/15/2020 to 4/26/2020, following the same steps as the previous section. Print the report for verification if needed.

Step 2: Use the PPP FTE Count report to calculate the FTE for the date range of your pay period that included 2/15/2020, using the period start and period end dates as the range and following the same steps as the previous section.

Step 3: Only if step 2 is greater than step 1 should you proceed to step 4, if not you stop here as you do not qualify for the FTE Reduction Safe Harbor.

Step 4: Use the PPP FTE Count to calculate your FTE on the earlier of either December 31, 2020 or the date this application is submitted.

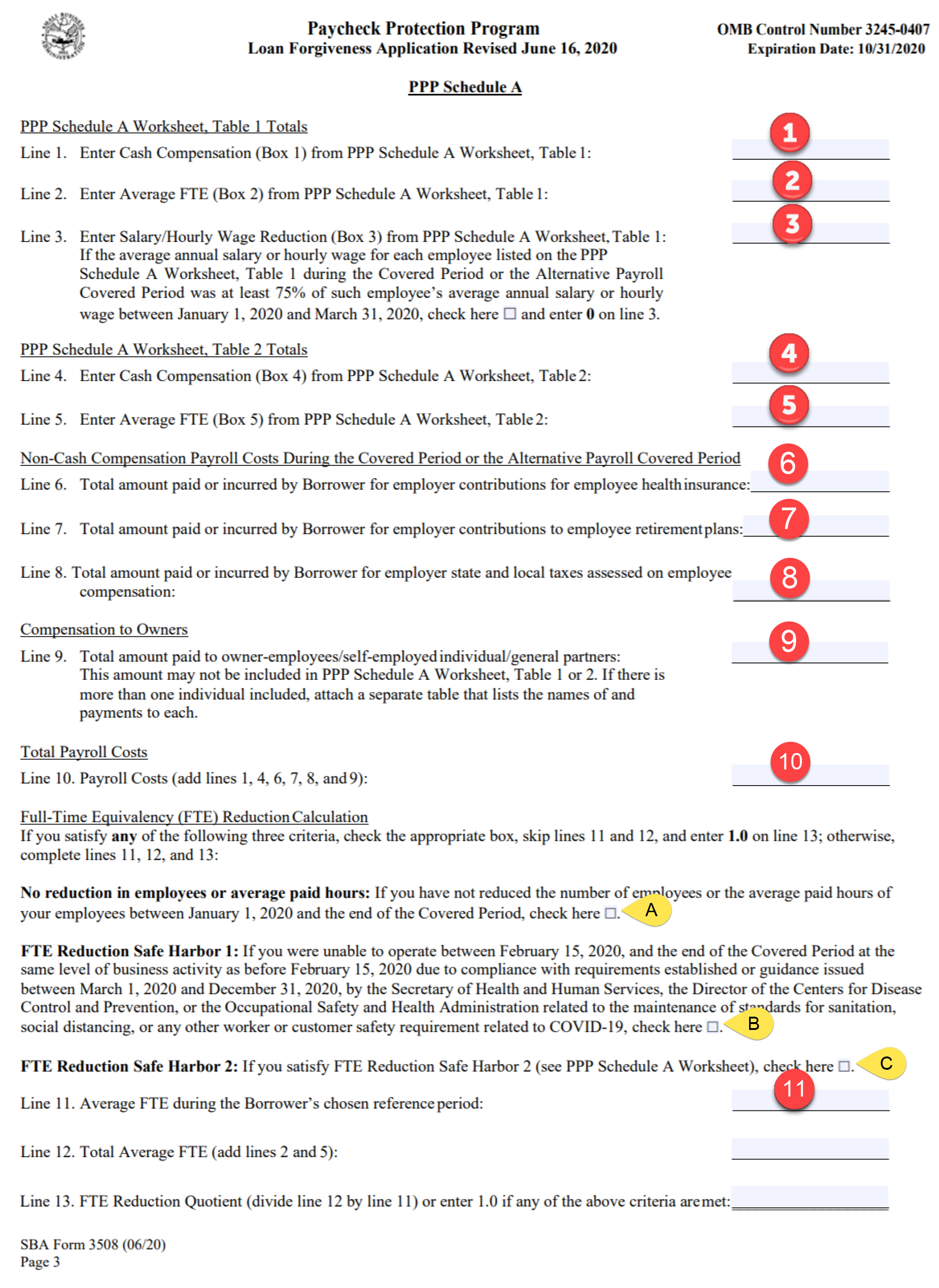

PPP Schedule A:

The data for PPP Schedule A derives from the Schedule A Worksheet Table 1 and Table 2. The details of how to derive the data correctly are provided in the PPP Schedule A Worksheet section of this article.

How it looks on the form:

How to get the info:

Lines 1 – 3: Table 1 Box 1, Box 2, and Box 3

The info here is in the Schedule A worksheet which you have already filled out in the previous step. However, we are showing you where to find it in our software so that it's clear how to obtain the data.

- Enter Cash Compensation (Box 1) from PPP Schedule A Worksheet, Table 1

- Enter Average FTE (Box 2) from PPP Schedule A Worksheet, Table 1

- Enter Salary/Hourly Wage Reduction (Box 3) from PPP Schedule A Worksheet, Table 1 However, see Salary Wage/Hourly Wage Reduction for certain cases where you need to add back salary amounts.

Notes:

- Each Box is at the bottom of Table 1, referenced by a key.

- To make edits on this worksheet, export to XLSX or CSV and you can modify it with your spreadsheet program.

- To print a verification report, press <ctrl>+P on your keyboard to print this report as verification documentation.

Lines 4 – 5: Table 2 Box 4 and Box 5

- Box 4 (Cash Compensation) and Box 5 (Average FTE) is on Table 2. The reference key is color-coded.

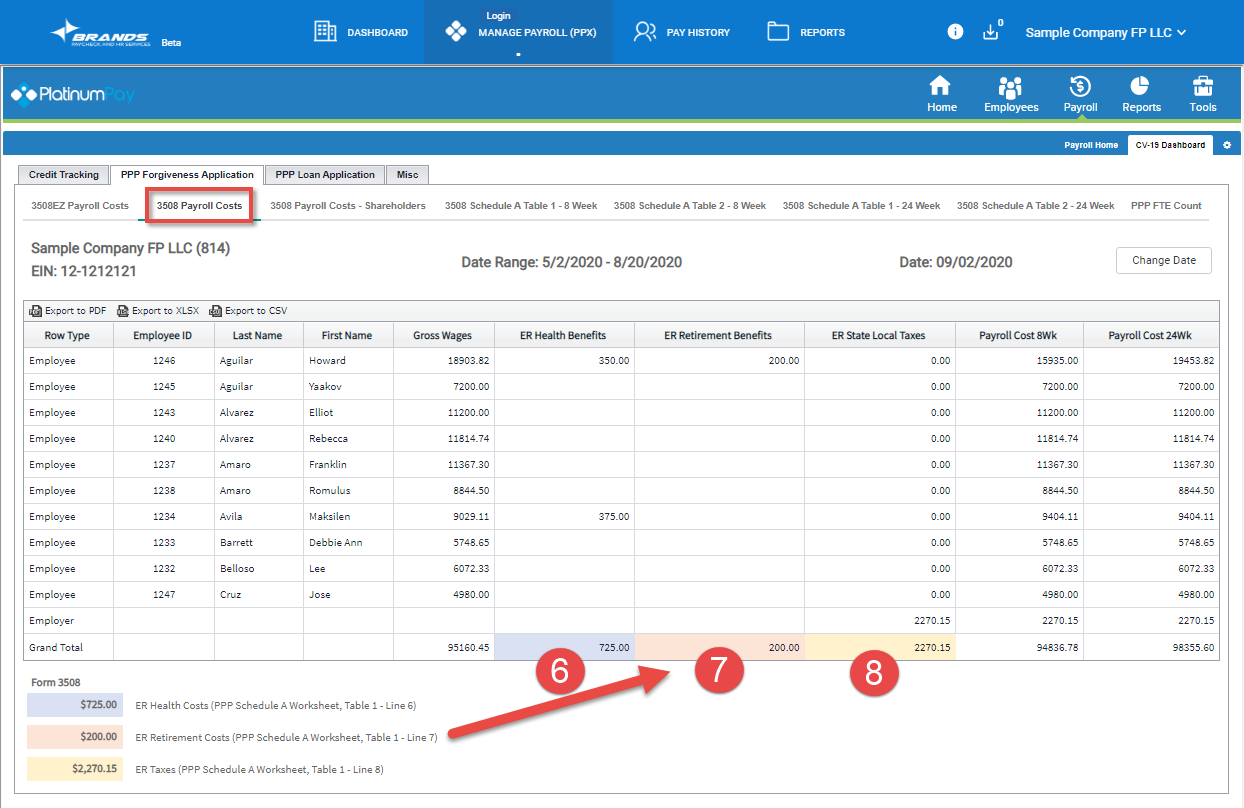

Lines 6 – 8:

The information for these 3 lines is in the 3508 Payroll Costs tab within the CV-19 Dashboard.

- Enter the total amount of the employer contribution to the health insurance premiums paid. If you record it in payroll via memos, we show the info here. Otherwise, you can get it from your insurance premium statements.

Notes:

- Do not include the employee portion as they are included in the cash compensation of the employee.

- Do not include premiums paid for an employee who is also a shareholder, where their portion is to be included in cash compensation, as in those cases they will be included in line 9.

- Enter the total amount of the employer contribution to employee retirement plans, typically called an employer match. If you record it in payroll via memos, we show the info here. Otherwise, you have that information elsewhere.

Note:

- Do not include matches paid for a general partner, where their portion is to be included in cash compensation, as in those cases they will be included in line 9.

- Enter the total state and local employer taxes for the period.

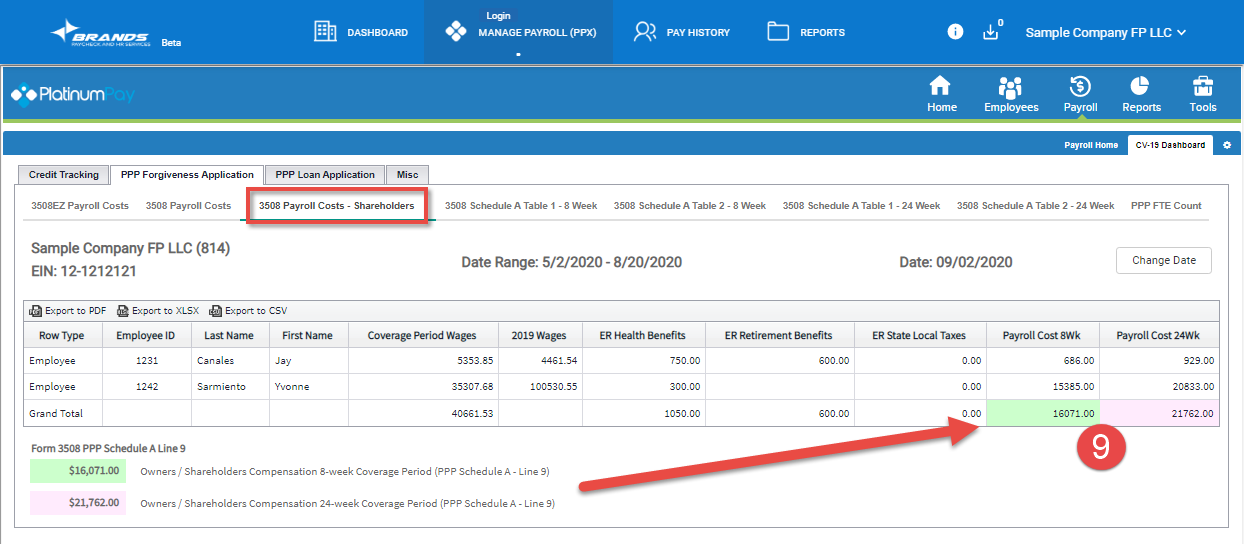

Line 9:

The information for this is in the 3508 Payroll Costs - Shareholders tab.

The employer health insurance premium and the employer retirement match amounts to be included as cash compensation is to be included in line 9 subject to the limitations for each individual within line 9.

Important Note: The health insurance paid for S-corporation employees with at least a 2% stake in the business, including for employees who are family members of an at least 2% owner, are included in the cash compensation and in the case of shareholders with a stake of 5% or more are subject to the limit on cash compensation of owners. Accordingly, if the cash they were paid reached the limit you should not add their health insurance in box 9.

For more details on this, see Owner/Company Shareholder.

Line 10:

- This is just the sum of lines 1,4,6,7,8 and 9.

Checkboxes A - C:

Checkbox A: If there was no reduction in employee count between January 1 and the end of the covered period: Check here, then enter 1 in line 13.

Checkbox B: If the reason your reduction in FTE is simply due to Covid-19 government health or safety agencies compliance requirements issued between March 1 2020 and December 31 2020 that prevent you from operating at the full level of business as you were operating at Feb 15, 2020: Check here, then enter 1 in line 13.

Checkbox C: If your company satisfied the safe harbor 2 test which you did on the schedule A worksheet: Check here, then enter 1 in line 13.

Line 11:

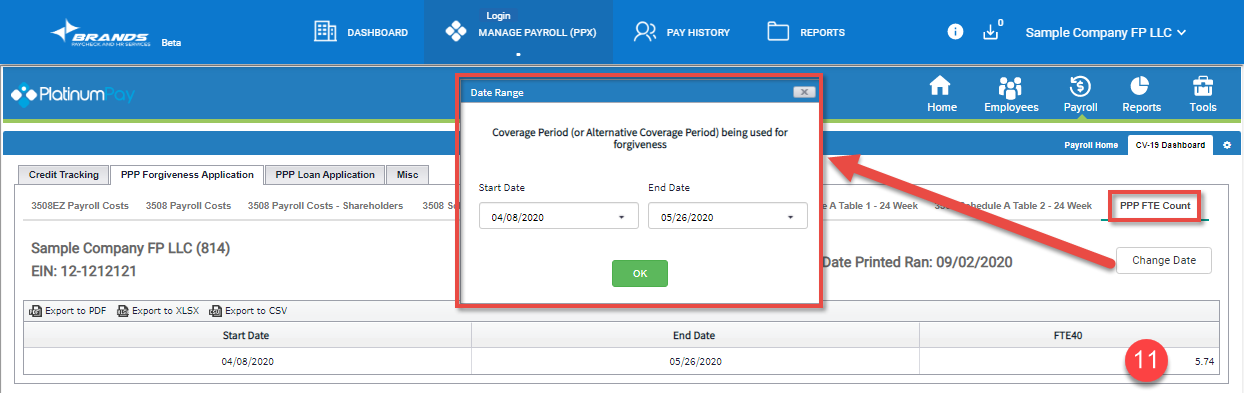

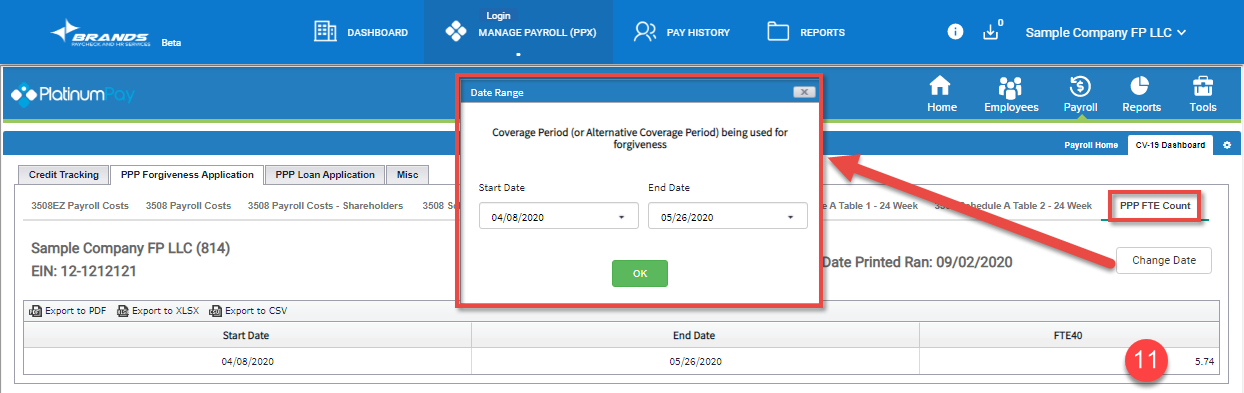

- To get average FTE for the chosen reference period, run the PPP FTE Count report for the specific date range. The FTE Count Report will calculate your Full Time Equivalency based on the date selected.

- Run the PPP FTE Count report by clicking on that tab.

- Click the Change Dates button and enter the date range needed.

- The value in the FTE40 field is the value you use for “Employees at Time of...”

- On your keyboard, press <ctrl>+P to print this report as verification documentation for each time period.

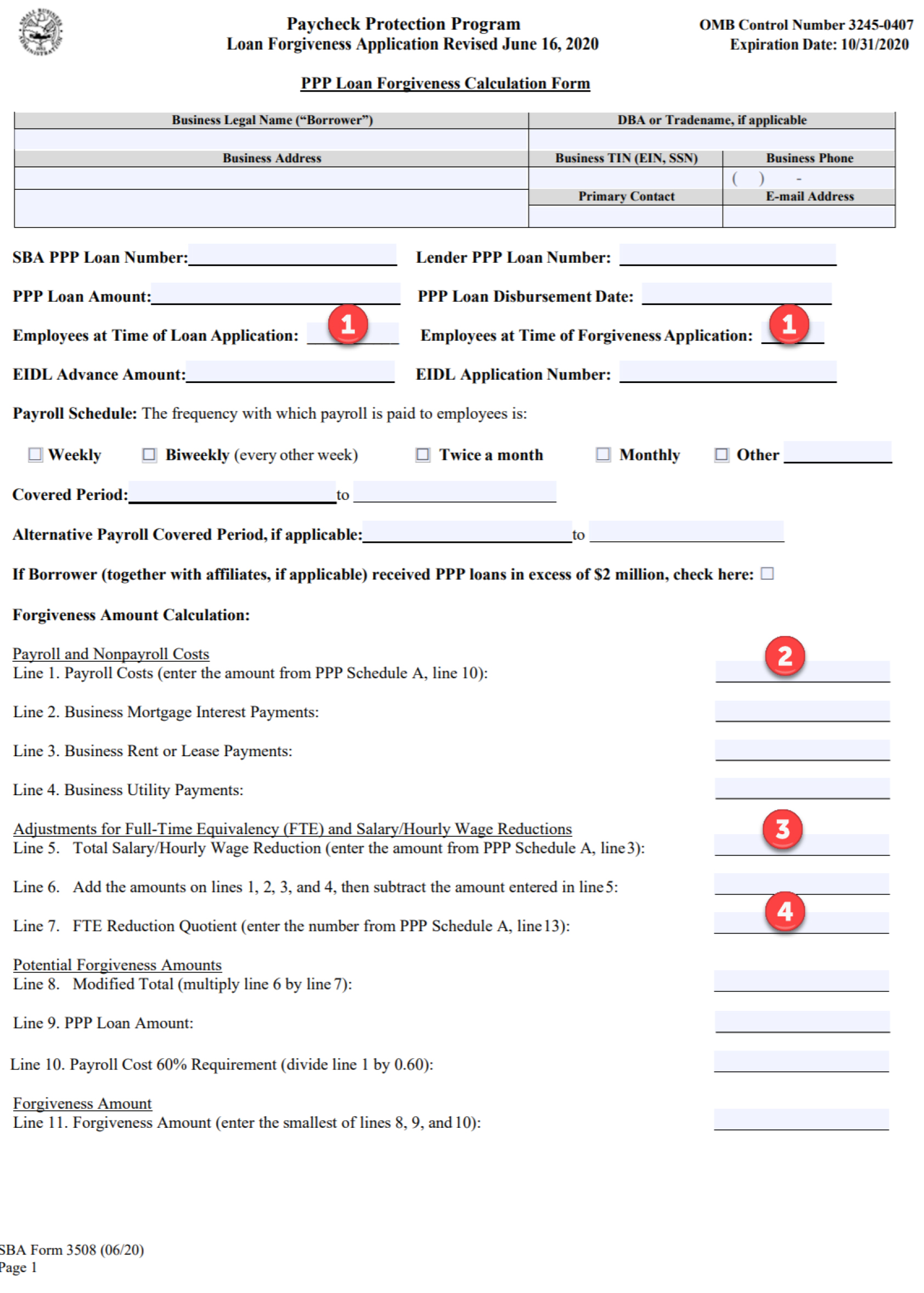

Forgiveness Calculation Form

Following is the PPP Loan Forgiveness Calculation Form and corresponding numbers to explain the data we provide.

How it looks on the form:

How to get the info:

Employees at time of loan application and time of forgiveness application

To get employees at time of loan application and forgiveness application, run the PPP FTE Count report for each date range. The FTE Count Report will calculate your Full Time Equivalency based on the data selected. We suggest running the report for the month, to ensure all your employees are counted (this is not required and you can run it for a smaller data range; only pay dates in that range will be counted).

- Run the PPP FTE Count report by clicking on that tab.

- Click the Change Dates button and enter the date range for the month you applied for the loan. For example, if you applied for the loan in April, use 4/1/2020 to 4/30/2020 as the date range.

- The value in the FTE40 field is the value you use for “Employees at Time of...”.

- On your keyboard, press <ctrl>+P to print this report as verification documentation for each time period.

- Repeat these steps for Loan Application and Forgiveness Application date ranges.

- Line 1 on this document is from PPP Schedule A, Line 10.

- Line 5 on this document is from PPP Schedule A, Line 3.

- Line 7 on this document is from PPP Schedule A, Line 13.

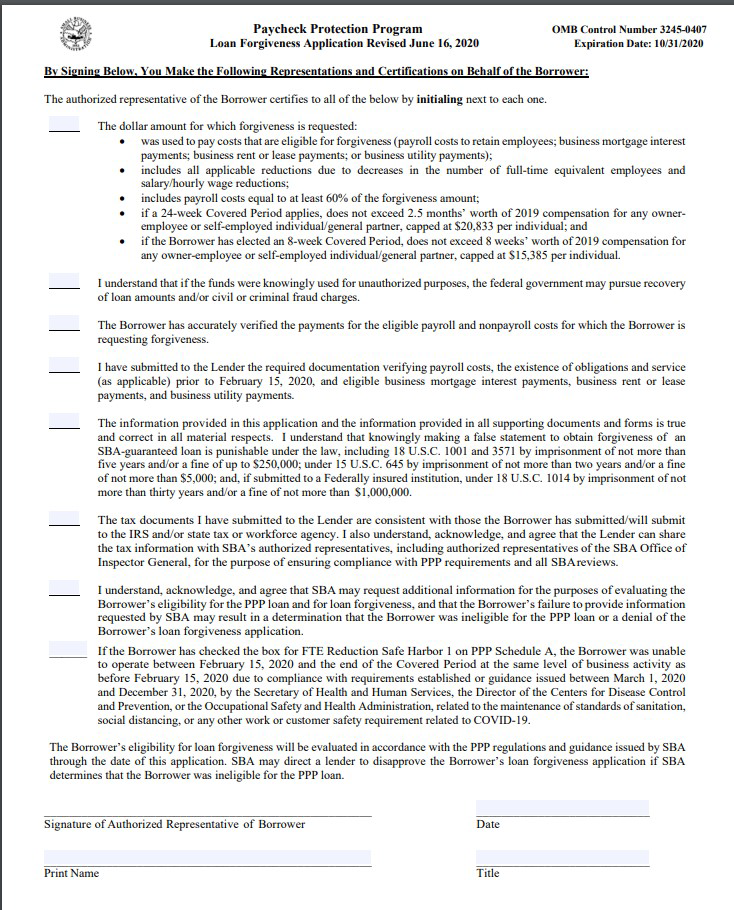

Borrower Certifications

In this section, the borrower is certifying that all the information provided is correct and that they are aware of the consequences of providing false information in this form.

Review each of the questions and check them all off. Then sign the document.

How it looks on the form:

--

Special Considerations

In this section, we cover many aspects of the form that have been intentionally excluded from the step by section of this article so that the reader is not interrupted and can focus on the items relevant to them.

- Can Your Company Use 3508S?

- Can Your Company Use 3508EZ?

- Payroll System Setups/History

- FTE Reduction Exception

- Salary Wage/Hourly Wage Reduction

- Owner/Company Shareholder

Can Your Company Use 3508S?

On October 9, 2020, a more simplified form has been released by the SBA to a narrow group of borrowers. That is borrowers with a PPP loan amount of 50,000 or less.

While those borrowers still need to ensure that the money was spent correctly, timely, and subject to the various caps for owners and employee compensation, this new form and rule relieves those borrowers from having to reduce forgiveness if they had a reduction in payroll, or have reduced any employees’ compensation during the Covered Period.

Borrowers that use this form, are also able to submit much less documentation during the loan forgiveness application process than borrowers using the other loan forgiveness applications.

Accordingly, before you start gathering the data and getting ready to submit your application you will want to check if you are one of those borrowers that is eligible to use the Form 3508S (PPP Loans Under 50K)

Can Your Company Use 3508EZ?

Before you proceed with this form which is the long version of the application you will want to determine if you are required to use form 3508 and you don't have the option to go with form 3508EZ which is much simpler and easier to complete. If you can answer yes to one of the following 3 options you can go with the 3508EZ, if that is the case go to PPP Loan Forgiveness: Step-By-Step Guide Form – 3508EZ:

- You are self-employed or an independent contractor, OR

- You are a sole proprietor with no employees, OR

- You didn’t reduce salary or wages for any employee by more than 25% during the covered period. If you qualify under this requirement, you also must meet one of the following 2 requirements:

- You did not reduce the number of employees or average paid hours of employees from January 1, 2020, through the end of the covered period, OR

- You were unable to maintain the same level of business activity as prior to February 15, 2020 during the covered period.

If you cannot answer yes to any of the above 3, you will need to complete the regular (long version) of the form 3508 PPP forgiveness application, the step by step of form 3508 is outlined in this article.

Payroll System Setups/History

To ensure that the data we produce is complete and valid, you need to ensure that certain employee setups are correct. Some of these you might not have needed in the past, but they are important now as many figures are derived from them.

Pay Status - If you have salaried employees that have no hours recorded on a per payroll basis, you should change them to Salary.

Shareholder - If some of the shareholders are paid via the payroll system, set them up as a shareholder in their employee profile.

Hourly Employees - If you have hourly employees that you do not record the hours in the system for during payroll, your FTE count will be incomplete and you will need to get that through other means as the data is not available in the payroll system.

Salaried Employees - If you have salaried employees which do not work 40 hours a week and you do not record their hours during payroll in the system, you will need to ensure that you account for that correctly in the various employee counts.

FTE Reduction Exceptions

On one before the last line of Schedule A Worksheet Table 1 in the Average FTE column, you add employees to your employee count if your employee count was reduced and their position was not filled yet and one of the following 3 conditions are met.

- Any position in which the employer offered the job back to the employee who was holding that position on 02-15-2020 refused and the employer was unable to find a similarily qualified replacement for the position at issue on or before Dec 31, 2020.

- Any position in which the employer made a good faith offer to restore the reduction in hours at the same hourly or salary rate during the covered period and the employee rejected the offer.

- Any employee who during the covered period was either (a) fired for cause, (b) voluntarily resigned or (c) voluntarily requested and received a reduction of hours

This is information which only you would have as those types of information are not reflected in the payroll software. As such, if you have an issue with the employee count you would have to further analyze the data so that you can determine if you need to add employees due to the existence of one of the above 3 scenarios.

Important Note: Since the reduction exception line only exists in table 1, which is for below 100K employees, you need to ensure that if you have a reduction exception for the over 100K employee list they are added to the reduction exception in table 1, as all reduction exceptions belong in table 1.

Salary Wage/Hourly Wage Reduction

As outlined in the Salary/Hourly Wage Reduction section on page 4 of the PPP Loan Forgiveness Application Table Instructions, finding the answer to this question on a per-employee basis is complex as it requires many comparisons and calculations so that you can determine if there is a salary reduction.

Before digging into the details, most employers should be able to answer this very easily as the question here is:

- Did you reduce the "salary rate" or the "hourly rate" for employees for the hours that they "worked" during the coverage period? If the answer is no (as we expect the case to be by most employers) they simply have no salary reduction whatsoever.

If the answer is no, you can just zero out all the salary reduction amounts without going through complex calculations to figure this out, as there was no salary reduction.

If the answer to the above is yes and you therefore need to calculate the salary reductions, continue reading.

We have done the entire calculation for you. Our report outlines up to which step we calculated for the employee at issue, which led us to the determination we made.

However, it is important to note that:

- For hourly employees: If hours were entered in the system whenever payroll was entered, the data is complete.

- For salaried employees: We are running with the assumption that there was no reduction in hours worked. If you know that there was a reduction in hours worked and that is the reason there was a reduction in salary amount, you will need to factor that in to determine whether there is, in fact, a salary reduction and how much the reduction was.

To calculate the reduction manually, refer to page 4 of the PPP Loan Forgiveness Application Table Instructions under Salary/Hourly Wage Reduction. Columns Step1A, Step1B, Step1C, Step2A, etc. correspond to the instructions. The Last Step Completed is where the formula ended to get the answer for this column.

Owner/Company Shareholder

An owner or shareholder of a company has special rules as it relates to what and how much of what was spent on their behalf is forgivable. The following are the highlights.

Note: Per SBA Guidance issued on 08-27-2020, an owner of a C or S corporation with less than 5 percent ownership stake is treated as a regular employee and is therefore not subject to this limitation.

- The forgivable amount of compensation paid to an owner/shareholder is limited. If you use an 8 week period, it is the lesser of $15,385 or the eight-week equivalent of their 2019 wages. If you use a 24 week period, it is the lesser of $20,833 or 2.5 months equivalent of their 2019 wages.

- The amounts paid by the company for the health insurance cost of an owner/shareholder is generally included in their cash compensation. If you already entered them in the payroll system as their cash compensation, do not add that again in box 9. If you did not enter them in payroll as their cash compensation, you can add it on line 9 but only up to the cap for shareholders (we show the info in the shareholder tab within the CV-19 Dashobrd but exclude them from the total cost that will be used in line 9 of Form 3508).

- The amounts paid by the company for retirement contributions (aka employer match) of a self-employed individual or general partner is included in their cash compensation. If you already entered them in the payroll system as their cash compensation, do not add that again in box 9 (we show the info in the shareholder tab within the CV-19 Dashobrd but exclude them from the total cost that will be used on line 9 of Form 3508).

Forms & Resources

Following is a list of documents and resources you might find useful.

Form 3508 - PPP Forgiveness Application (Long Version)

Form 3508 Instructions - Forgiveness Instructions (Long Version)

Form 3508EZ - PPP Forgiveness Application (Short Version)

Form 3508EZ Instructions - Forgiveness Instructions (Short Version)

Form 3508S (PPP Loans Under 50K)

Form 3508S Instructions (PPP Loans Under 50K)