Section 1106 of the CARES Act provides forgiveness of the PPP loan received under Section 1102 of the CARES Act. If you have received a PPP loan, you must ensure that you are using the loan only for allowable expenses. Since the Treasury Department outlines many factors that will affect the amount that can be forgiven, you will want to ensure that you take all reasonable measures to maximize that amount.

While some guidance is still evolving, employers need to know what to do now, given the information currently available. Here we summarize the items to monitor, as well as the intuitive tools we have provided within our Covid-19 Dashboard so that you can easily check on how you are doing and adjust them in time to maximize your loan forgiveness amount.

Important Update: On June 3, 2020, the Senate passed H.R.7010 - Paycheck Protection Program Flexibility Act of 2020. As its name suggests, it provides much more flexibility to borrowers and is also expected to change the loan forgiveness application items. We have outlined for you a Summary of Paycheck Protection Flexibility Act. Rest assured we are on it and we are evaluating the additional items needed to easily fill out the loan forgiveness application. As soon as the SBA or Treasury Department provides updated guidance as to how the loan forgiveness application is changed as a result of this act, we will modify the loan forgiveness tools and ensure that you have all the necessary items so that you can easily fill out the loan forgiveness application.

Jump to:

- What can I spend the money on?

- How much will be forgiven?

- Reductions in allowable forgiveness

- Summary

- Covid-19 dashboard items

- Links & resources

What can I spend the money on?

You may only use the money for the following items:

- Payroll costs

- Additional wages paid to tipped employees

- Interest on a mortgage

- Rent on a lease agreement

- Utility payments

At least 60% of your loan must be spent on payroll costs only, and 40% can be spent on the other expenses.

Update: H.R.7010 - Paycheck Protection Program Flexibility Act of 2020 which was signed into law on 06-05-2020, changes the percentage of payroll to 60% and 40% on other expenses, for more on this see Summary of Paycheck Protection Flexibility Act.

How much will be forgiven?

You are eligible for loan forgiveness of up to 100% of the principal loan received, up to the amounts you spend on any of the eligible items (subject to limitations outlined further) during the 24 week period. The 24 week period starts on the day you received the first disbursement of funds from the lender.

To maximize the amount eligible for forgiveness, you need to ensure the following:

- You are only using it for forgivable expenses.

- You use up the funds during the first 24 weeks.

- You use 60% of the loan proceeds for payroll cost and no more than 40% on the other expenses.

- You only calculate up to 15,385 of gross payroll per employee (the excess amounts paid per employee is not forgivable).

- You maintain the employee headcount.

- You don’t reduce with 25% or more, the wages of employees earning less than 100,000 annually.

Update: H.R.7010 - Paycheck Protection Program Flexibility Act of 2020 which was signed into law on 06-05-2020, changes the percentage of payroll to 60% and 40% on other expenses, extends the period to spend the funds from 8 weeks to 24 weeks, and gives greater flexibility on maintaining the employee headcount and more, for more on this see Summary of Paycheck Protection Flexibility Act.

Reductions in allowable forgiveness

In addition to using the funds for the allowable expenses, your loan forgiveness will be reduced to the extent that your headcount was reduced when compared to your headcount in the lookback period or you reduce any employee wages by more than 25%. Details are outlined further.

Maintaining employee headcount

Your forgiveness amount equals your total payroll costs multiplied by the average number of full-time and Full-Time Equivalent (FTE’s) employees you retained for the eight weeks following the date of your loan origination divided by the lower of:

1) the average number of full-time employees and FTE's you had per month from Feb. 15 to June 30, 2019; or

2) the average number of full-time employees and FTEs you had per month from Jan. 1 to Feb. 29, 2020; or, if you are a seasonal employer, the average number of full-time employees and FTEs per month you had on staff from Feb. 15 to June 30, 2019.

Employee Reduction Example:

- Loan Amount Received = $500,000

- Lookback Period Employee Count = 200

- Current Employee Count = 100

- Loan Forgiveness Percentage = 100/200 = .5

- Loan Forgiveness Amount = $500,000 * .5 = $250,000

Special Notes:

- If an employee was laid off at first, and then was offered to be rehired for the same salary/wages and the same number of hours and the employee refused the offer, the employer is deemed to have employed the employee and the headcount is not reduced by the fact that that the employee did not work. To qualify for this exception, the borrower must have made a good faith, written offer of rehire, and the employee’s rejection of that offer must be documented by the borrower.

- Employee count for purposes of forgiveness is different than for purposes of eligibility to apply for the loan. For eligibility purposes, each employee is counted as one. As such, if an employer has 450 full-time employees and 51 part-time employees, they are ineligible to apply for the loan as they have more than 500 employees.

- When it comes to forgiveness, the full-time employees, as well as the (FTE’s) employees, are taken into consideration to determine your comparable period's employee count, as well as the 8 week period's employee count. The definition of an FTE is like for ACA purposes. That is, every 120 hours per month of work performed by your part-time employee is equivalent to one employee.

Update: H.R.7010 - Paycheck Protection Program Flexibility Act of 2020 which was signed into law on 06-05-2020, provides for greater flexibility to employers on maintaining the employee headcount and more, for more on this see Summary of Paycheck Protection Flexibility Act.

Maintaining wage levels

Your forgiveness will be reduced dollar for dollar for any reduction in wages of more than 25% for all employees earning less than $100,000 per year. That is; if you reduce total salary or wages for any employee during the 24-week period after the lender sent your PPP loan funds to you by more than 25% as compared to the most recent full quarter before the 24-week period, then each dollar reduced will reduce a dollar of your allowable forgiveness amount.

If reductions made between February 15, 2020 and April 26, 2020 are reversed by June 30, 2020, your loan forgiveness amount will not be reduced.

This forgiveness reduction does not apply to reductions associated with employees who had a salary or wages higher than $100,000 in 2019.

Summary

From the day you received the loan as well as during the 24 week period, you should keep these questions in front of your eyes and monitor them so that you can correct any item you identify that needs correction to maximize your loan forgiveness:

- Are you spending at least 60% of the PPP funds on payroll costs?

- Are you maintaining your FTE averages? If not, should we hire/rehire some employees?

- Have you reduced any employee’s wages by more than 25%?

- How else are you spending the money? Are these PPP-approved expenses?

- How much of the PPP funds do you have left? How will you use these funds?

- What adjustment should we make so that 60% of the funds are spent on payroll costs?

Covid-19 dashboard items

We at Brands are committed to assist you with compliance and provide you tools and reports that your company needs as new requirements or needs arise.

For that reason, we have created the Covid-19 Dashboard where you can manage all Covid-19 related items.

The following icons within the Covid-19 Dashboard will be useful for your ongoing monitoring of the funds used for payroll costs that will be forgivable as well as the current FTE counts versus the lookback period's FTE count.

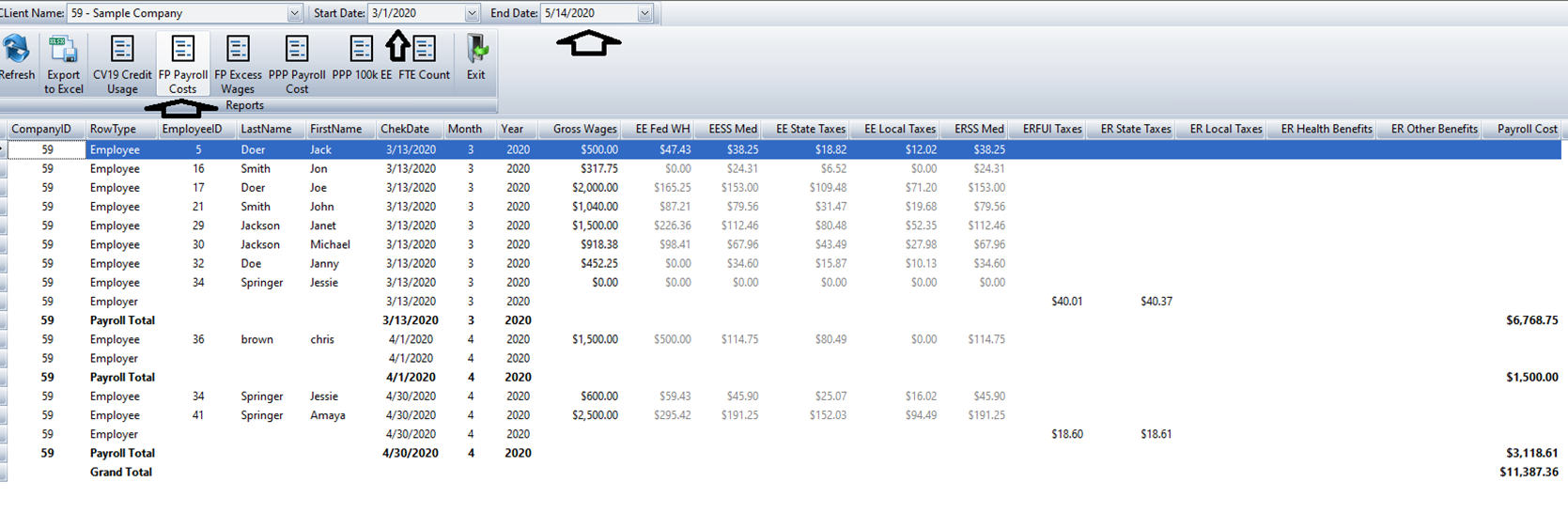

Payroll Cost

For the payroll cost, use the FP Payroll Cost icon. Adjust the start date to the date your loan was funded and the end date to the last day of the 24 weeks.

Here you will be able to see the accumulated payroll cost per payroll, per month and a grand total. The total cost contains only the amount that can be eligible for forgiveness. That is, the gross + ER state and local taxes + any ER benefits paid in addition to the employee’s gross.

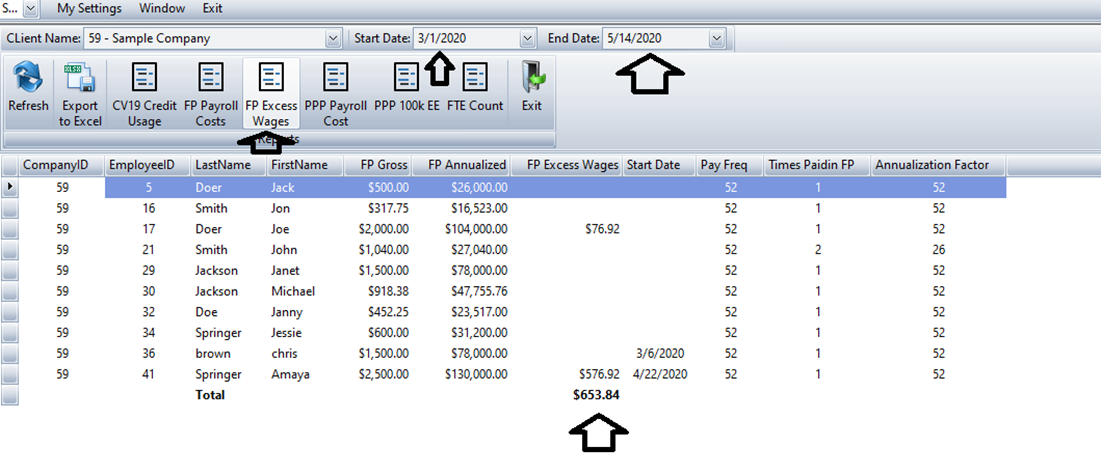

Excess Wages

For the excess wages, use the FP Excess Wages icon where you can see the prorated excess wages which will be reduced from the total cost when applying for loan forgiveness.

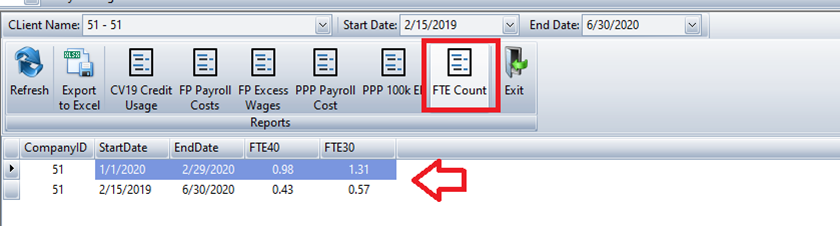

FTE Count

To evaluate your employee count in the lookback period, use the FTE Count icon. Adjust the date range as applicable to your company and then compare and see which range produces the lowest amount of employees. Compare current employee count to the lowest lookback period employee count.

Links & Resources

Following are links from government agencies you might find helpful:

Treasury Department PPP Resource Page